-

PAY Plantation®

PAY Plantation®

Payment Gateway.Send and Receive Money.

Start Accepting Payment online using PAY Plantation®LEARN MORE

Sign up for merchant account and start onboarding sales immediately.

TRUSTED BY Numerous Happy Business Owners.

Integrate PAY Plantation® API plugin interface within your website seamlessly and start receiving payment immediately.

Get StartedSecured and simple ways to receive payments online using Cross Border transfers, ACH, Wallet to Wallet, Bank transfers, etc.

Get StartedAnti-fraud and AML monitoring. Payment gateways hosted, ensure PCI DSS compliance and secured transactions.

Get StartedPAY Plantation® work to keep your account more secured & reliable, while you focus in growing your business, enjoy safe payments.

Get StartedAs you may know, most charitable non-profit organizations rely upon the generosity of donors for some or all of their funding. Consequently, fundraising is an activity of major importance to the charitable nonprofit community.

Donation-based fundraising is generally legal, but it's subject to regulations that vary by jurisdiction. In most places, non-profits, charities, and individuals can engage in donation-based fundraising activities if they comply with relevant requirements, laws and regulations that apply in their location where the fundraising is held.

Fundraising refers to the process of gathering voluntary contributions of money or other resources, typically for a charitable, nonprofit, or political cause. It involves soliciting donations or investments from individuals, businesses, organizations, or governments to support a specific project, initiative, or organization.

Pay Plantation® is a versatile fundraising platform that allows organizations, churches, and individuals to collect charitable donations through our platform. The campaign creator can share their donation campaign on social media, as well as through emails. Our donation-based platform supports recurring donations payment and integrated with seamless ACH and credit card payment capability.

When choosing a fundraising platform, consider factors such as fees, payment processing options, crowdfunding model (reward-based, donation-based, equity-based, etc.), ease of use, and the platform's specific features that align with your fundraising goals. Pay Plantation® is a donation-based platform, and we offer the lowest fee in the industry.

Start fundraising today.

Are you in need for fundraise?

Pay Plantation® payment gateway donation - fundraise solution feature is used for raising any kind of charitable funding online. Merchant users can create a campaign which will be visible to other users inside and as well as outside of the Pay Plantation platform for the merchant user donation needs.

The campaign creators can view their donation details, transaction list in the dashboard, and more. And they can share the campaign on social media, as well as on their website.

Register, create donation campaign, and start fundraise immediately..

Start fund-raise today

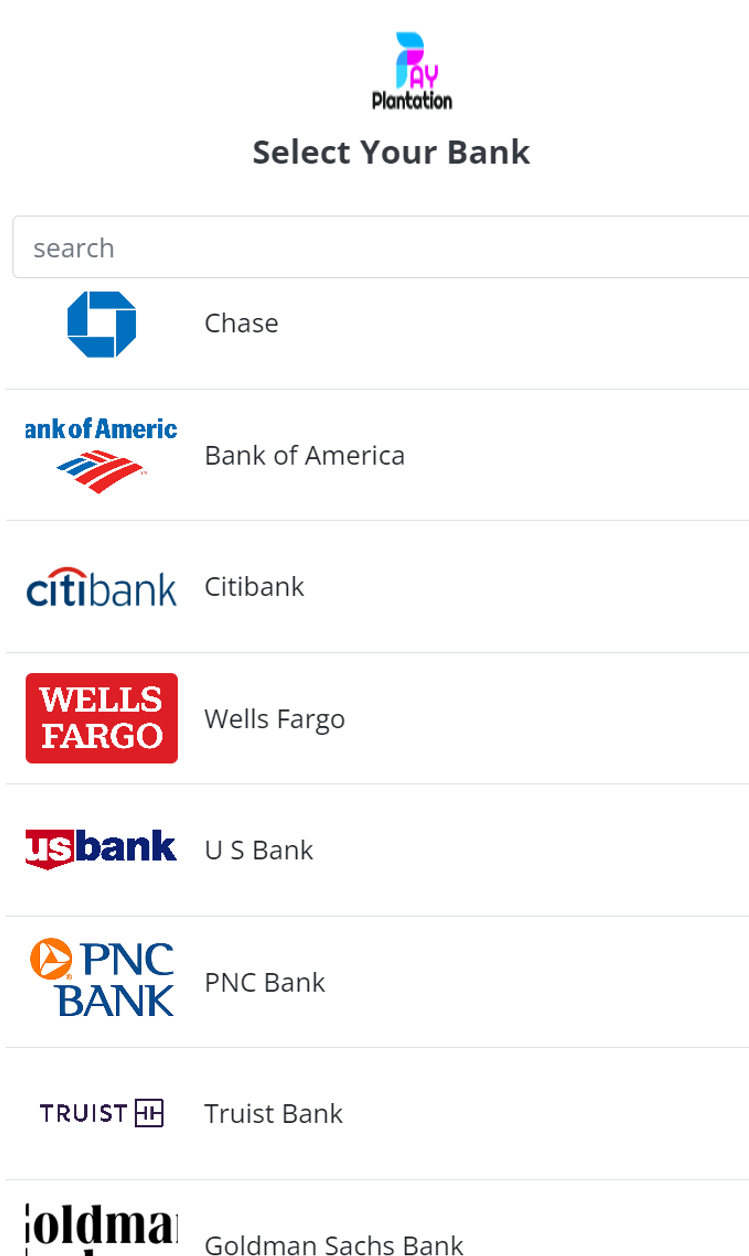

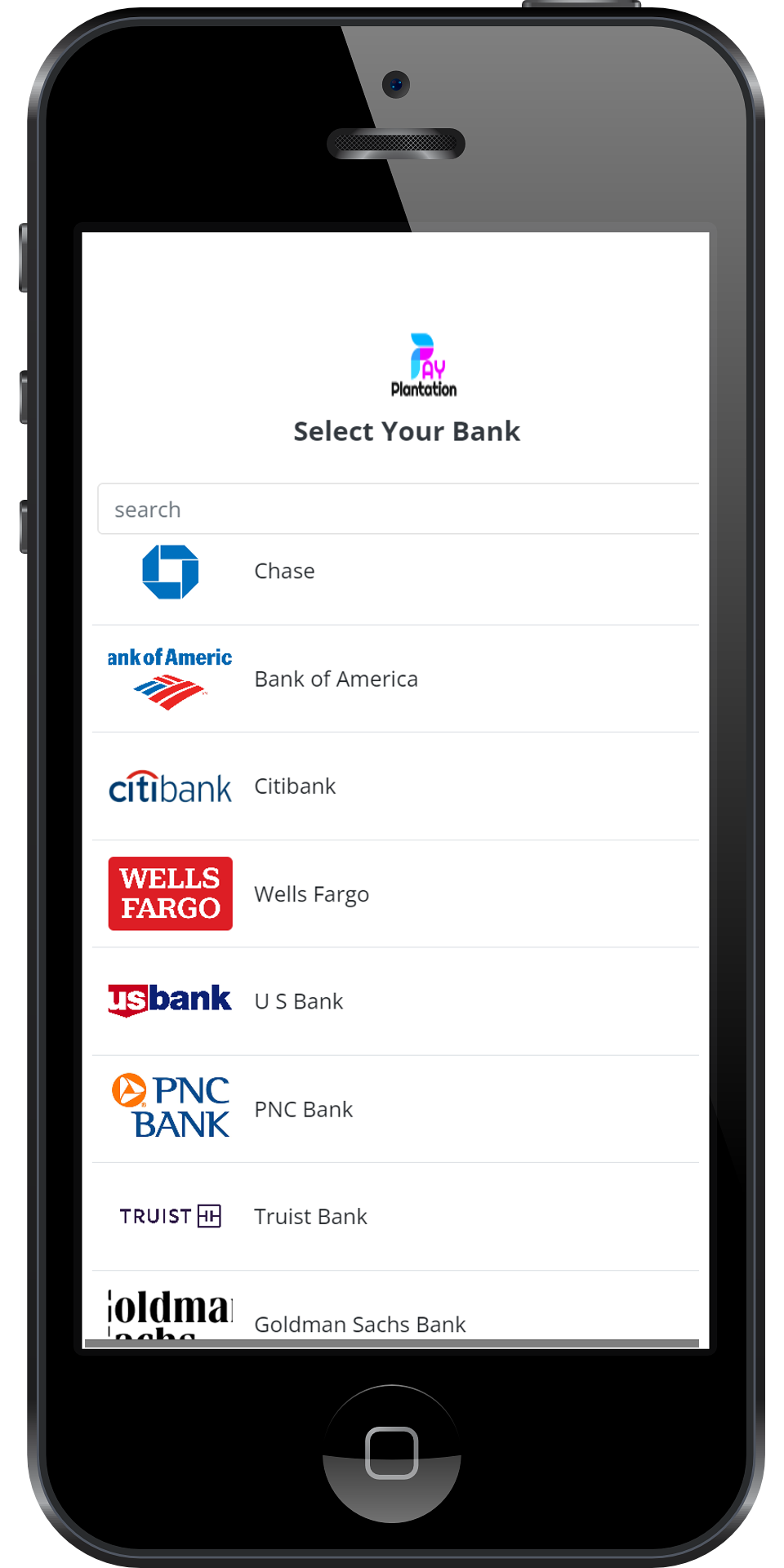

Integrating PAY Plantation® - Payment Gateway Rest API plugins to your website, platform, webpage, blog, and social network channel are easy as 1, 2, 3. We're a payment processor, digital wallets, money management technology company that value your business payment processing and billing needs. Set up business payments in minutes.

PAY Plantation® has developed numerous Application Programming Interface (API) for most popular Content Management System (CMS), E-Commerce Websites, Customer relationship management (CRM), Shopping Cart, and Social Network platforms for your convenience. We're connected to all banks and financial institutions in United States.

Send and Receive money from your PAY Plantation® wallet to another user on our platform wallet within seconds. Safe and Secure!

PAY Plantation® Payment Gateway Features.

User can create Merchant account. Start Accepting One-Time and Recurring Payments using PAY Plantation® Gateway API.

Get Started

Connect your sites and services via our Rest API plugin and start accepting payments. Our API's provide real-time transactions, tracking, and reporting.

Get StartedUser can create payment form that can be used to sell product and services in user website. Also, Payment link can be sent to your customer via email or SMS.

Get Started

Non-profit organizations, charities, Church, and individual can create just-cause fundraising campaign. Users and donors will be able to make donations to the campaign.

Get StartedIt's possible to send and request money from friends & family. The request receiver can approve or decline it. Users can easily access their money once login.

Get StartedUser can make deposit into PAY Plantation® Wallet, also have the ability to withdraw money directly to their bank account. And or use the Wallet balance to pay vendors and merchants.

Get StartedEasily withdraw money from your PAY Plantation account balance seamlessly to your designated Bank account - ACH. Your account balance is viewable at the dashboard.

Get StartedUsers can raise disputes against any merchant through the Dispute option, if user have any claim issue about their product or services purchased.

Get Started

PAY Plantation® is PCI-DSS, PSD2, GDPR/CCPA compliant. We actively stay up to date with global, national, and local payment, data privacy, and tax regulations compliant. We are the National Automated Clearing House Association (NACHA), affiliate member. NACHA is the organization that governs and regulates money-movement in USA.

Adding money to your Pay Plantation wallet is easy. Firstly, login to your Pay Plantation account, then click on the 'Deposit Fund' menu on the left side of your dashboard. Select the currency, enter the amount you would like to add and navigate to success. Pay Plantation is a payment service provider, a payment gateway enabling all companies to accept payments and individuals to make purchase payments to vendors.

Payment service providers enable business owners to securely accept online payments using their payment gateway infrastructure. Pay Plantation is one of the recognized payment service provider platforms in United States.

We're affiliated and partnered with ...